I’m getting flashbacks. Not good ones. Financial ‘engineering’ was a feature of the world’s last two financial crises. In the TMT bubble collapse, Enron used its stock as collateral in long-term contracts or asset sales which were described as “circular hedging transactions”. The goal or impression sought was to mitigate risk but ultimately all risk was really tied to the Enron share price. In the credit crisis of 2008/2009, new ways of packaging property debt with a bewildering array of acronyms (CLO, CMO, RMBS etc) were supposed to insulate risk within different tranches. Until, they didn’t.

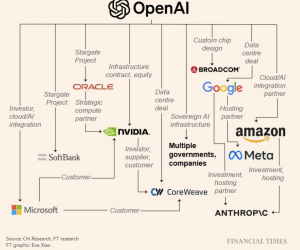

Now, I’m reading about new ways to finance the AI boom and, again, the risks keep coming back to a very narrow collateral pool. The word “circular” is back and one name keeps cropping up; OpenAI. My newsfeed has been bombarded with multiple graphics from Bloomberg, Goldman Sachs and The Financial Times (see below) illustrating this circularity accompanied by headlines stating that OpenAI is at the centre of a $1 trillion AI infrastructure spending boom. And, I thought they were just building a chatbot (ChatGPT).

Here’s a few things you might have missed about OpenAI….

A recent funding round valued OpenAI at $500 billion, the world’s most valuable private company, but….

It generates NO cash. Latest figures for H1 2025 reveal revenues of $4.3 billion while incurring a net loss of $13.5 billion. Yep, it’s losing more than 3 dollars for every dollar of sales it generates.

OpenAI has signed up to $1 trillion of deals with the likes of Oracle ($300 billion), Nvidia ($100 billion), AMD ($80 billion) and Coreweave ($22 billion). The Stargate project alone is a $500 billion infrastructure project.

OpenAI’s core product, ChatGPT, has built a weekly user base of 800 million people.

Now, let’s return to the deals. I’m not sure the graphics of circularity really capture what’s going on. In recent weeks the world’s most valuable company, Nvidia, announced a $100 billion investment in OpenAI. In return, OpenAI will buy Nvidia’s graphic chips (GPUs) as it builds out its data centre infrastructure. You can see the circular vendor-financing risk in that deal. However, in the last 24 hours OpenAI has announced a further deal with Nividia rival chip maker, AMD. I’m going to lean on Bloomberg’s excellent Matt Levine in imagining the language of current deal negotiations with the loss-making OpenAI.

OpenAI: We would like six gigawatts worth of your chips to do inference.

AMD: Terrific. That will be $78 billion. How would you like to pay?

OpenAI: Well, we were thinking that we would announce the deal, and that would add $78 billion to the value of your company, which should cover it.

AMD: …

OpenAI: …

AMD: No I’m pretty sure you have to pay for the chips.

OpenAI: Why?

AMD: I dunno, just seems wrong not to

OpenAI: Okay. Why don’t we pay you cash for the value of the chips, and you give us back stock, and when we announce the deal the stock will go up and we’ll get our $78 billion back.

AMD: Yeah I guess that works though I feel like we should get some of the value?

OpenAI: Okay you can have half. You give us stock worth like $35 billion and you keep the rest.

Levine is spot on. It has been bothering me for weeks now. CEOs in the tech world have spotted that a company’s share price goes up on the announcement of huge spending plans (not profits). In extremis, one could route the “value” of the share price gain to a cash-strapped customer like OpenAI. Funnily enough, AMD’s share price rocketed 35% on the OpenAI deal news adding $60 billion to its market value. And, so the merry go round continues. Sure enough, Nvidia, has responded to the behind-the-back dealing of OpenAI with rival AMD by announcing a $2 billion investment in OpenAI rival, xAI, owned by Elon Musk. The total funding round for xAI will be $20 billion but there’s a few extra ‘engineering’ twists. The $20 billion ($7.5 billion equity, $12.5 billion debt) is going into a special purpose vehicle (SPV – remember them?) which will buy GPU chips for xAI’s Memphis Colossus 2 data centre. The SPV, in turn, will rent out the GPU chips for 5 years, with the debt backed by the chips rather than the company. Hmmmm. The rent and SPV details should raise alarm bells.

The attraction of constructs like rent, leases and special vehicles is that it increases the complexity of an organization and also makes it more difficult to track the true returns (or not) of a company. Rent and leases are considered off-balance sheet items ie they don’t show up as DEBT on the balance sheet. To complete the circle, I’m reading about Oracle today and its astonishing $380 billion in revenue it will generate by renting out its cloud servers to OpenAI and other AI developers over the next 5 years. Oracle can’t afford a rent default. It is not cash rich like Google or Microsoft. In fact, its debt-equity ratio is a whopping 520%. Michael Cembalest at JP Morgan put it rather well…

“Oracle’s stock jumped by 25% after being promised $60 billion a year from OpenAI, an amount of money OpenAI doesn’t earn yet, to provide cloud computing facilities that Oracle hasn’t built yet, and which will require 4.5 GW of power (the equivalent of 2.25 Hoover Dams or four nuclear plants), as well as increased borrowing by Oracle whose debt to equity ratio is already 500% compared to 50% for Amazon, 30% for Microsoft and even less at Meta and Google. In other words, the tech capital cycle may be about to change.”

Change, yes. But some things never change in credit or investment cycles. OpenAI might be at the centre of a $1 trillion investment revolution driving stock prices ever higher. But, ultimately “other people’s money” will make its presence felt. Bloomberg is reporting that the amount of debt tied to AI has ballooned to $1.2 trillion. This makes AI the largest segment(14%) of the investment-grade market, surpassing US banks. That means more eyes and scrutiny on the circular world of AI. Bluntly, if a problem emerges it won’t be seen in the stock markets first. It will be in the bond markets with its army of credit analysts. As a final thought, and given the scrutiny applied to the track records of key entities in investment ecosystems, what must credit analysts think of OpenAI?

- As recently as 2023, the OpenAI CEO, Sam Altman, was fired, then re-hired.

- OpenAI co-founder, Elon Musk, is now a bitter and richer rival.

- The company is a strange governance hybrid with control residing in a non-profit Board.

- OpenAI and early backer, Microsoft, have been in dispute over their partnership terms.

- CEO Sam Altman was quoted this week in FT saying becoming profitable was “not in my top-10 concerns”

- Recent $100 billion investor in OpenAI, Jensen Huang of Nvidia, was not told about the deal with rival, AMD.

None of the above makes OpenAI a bad credit. But, with trillions of dollars of investment capital on the line any loss of confidence in OpenAI could spiral rapidly into a whole new circle of “engineering” PAIN.