WeWork really really doesn’t work. What a week it has been. The WeWork IPO has not just been pulled but its CEO, Adam Neumann, has also been yanked off the stage along with a number of other senior executives. WeWork’s mission to ”elevate the world’s consciousness” has elevated much much more. WeWork planned leases have been canceled, loans/bonds are being watched nervously and the investors are now putting private company valuations under a public reality microscope.

Another planned IPO, Endeavour, in the events/talent space has been pulled in New York and the much-hyped lifestyle franchise, Peloton, has had a difficult first few days trading since IPO. Current losses for public investors in Peloton are 13% after a couple of days but it could be worse. Teeth straightening play, SmileDirectClub, is generating very few investor grins as its share price has plummeted 44% in its first few weeks as a public quoted company. It will be argued that WeWork was the most egregious attempt to sell to “the greater fool” and was the sudden trigger for valuation fatigue and a halt to governance nonsense. However, this writer would suggest that the divergence between private funding froth and the greater transparency of public market valuations was running out of road over a much longer period of trading time.

Yes, public markets are not far off all-time highs in a US context but this narrative hides a more demanding environment for public markets in recent years. If US markets(big if) finish 2019 at similar levels as today the S&P 500 will have gone pretty much nowhere over a period of 2 years. No wonder the Orange Toddler Twitter machine is in super frustration mode. It could be worse, you could be an investor in Europe. The benchmark European index, the Stoxx 600, is actually trading at the same level as March 2015. Go East and weep at Groundhog Day for China whose markets have endured a round trip to nowhere since 2014!

Investors in the likes of Uber, Lyft and Slack will attest to public market debuts lacking in any joy. The simple truth is that valuation eventually does count and lends itself to Benjamin Graham’s assertion that in the long run the market is a weighing machine. The shorter-term popularity, voting machine approach to private equity unicorn valuations are now poised to give way to some serious discussions on valuations and governance. As we previously wrote, there will be real skepticism surrounding any “cult” founder stories and one suspects Adam Neumann’s humbling 169 mentions in WeWork’s IPO filing will be a high watermark for funding hagiography.

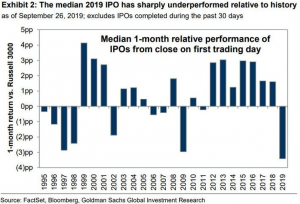

The good news for startups and younger companies seeking funds is that a solid story with a strong management structure and realistic financials will have less funding competition from “hot” concepts. This is capitalism. Creative destruction will create a cautionary tone for a while but ultimately ensure capital is properly allocated in line with more fundamental investment processes. The data suggests 2019 has provided an inflection point for private valuation excitement. The median IPO in 2019 has had its worst first-month performance since 2009. The S-1 filing documents for IPOs like WeWork can mislead but this chart certainly does not:

The good news for startup founders is that there is plenty of private capital out there and interest rates/yields for investors are currently at historic lows. So, there is plenty of interested investor ears. For those thinking about access to capital, one should consider crowdfunding as a good platform to learn and ultimately execute your own fundraising story. Equity crowdfunding does work. Contact us today to learn more about how Spark Crowdfunding can help your company grow.