The recently deceased actor, Brian Dennehy, once asked to stay the night in our house and we turned him away. True story. However, context and logistics are everything. Of course, we would have loved to tell the tale of hosting a Hollywood legend except there were already 25 Irish teenagers staying in our house during that J-1 summer of 1989 in Montauk, Long Island. So, it is no surprise that Dennehy’s death and oil prices (with a minus) over the past week did jog the memory and highlight all over again the importance of space irrespective of the opportunity.

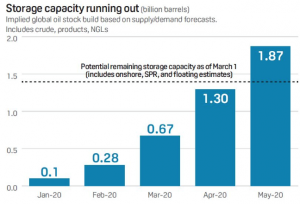

As US oil futures plunged into negative territory in recent days we were reminded that if there is no storage available you can’t even give away a bulky commodity. In fact, some contractual parties in the futures market were prepared to pay somebody, anybody $35 for each barrel of oil to be taken off their hands. Just think, if one could have taken delivery of a million barrels of West Texas oil there was a whopping $35 million payment to accompany that load. The problem as the following chart from energy consultant, Platts, shows is that the US market has maxed out on storage capacity:

Yes, that looks like we are rapidly approaching a stock build of almost 2 billion barrels of oil with storage capacity for closer to 1.5 billion barrels. The main driver of the stock build is CV-19 and the evaporation of oil demand. Think back to 2019 and daily oil consumption of 100 million barrels per day. Current estimates suggest we might be consuming 25 million barrels less, each day! To halt production would be very expensive hence the stock build and furious prayers to the Donald, Allah and Saint Christopher, the patron saint of travel. Hopefully, the rest of the world can follow China back to some sort of post Covid recovery phase but the decline of oil pricing power has been a multi-year trend.

Here are a few further thoughts on the decline in influence of carbon fuel producers:

- For consumers of energy, as individuals or as businesses, a collapse in fuel prices should be viewed as an enormous tax cut.

- In 1980 the oil sector accounted for 30% of US equity markets. It now accounts for less than 3% while the technology sector represents more than 23% of the market. Who said data was the new business fuel?

- Rogue states and despotic leaderships dependent on commodity markets can be vulnerable to sovereign debt implosions and civil unrest. Russia and Saudi Arabia are more fragile than perhaps financial markets and investors appreciate.

- Storage has hurt the oil markets temporarily but on a longer term view storage will be equally important to the emerging renewable/electric/battery powered economy. There is still much to be done to improve battery/storage technologies. One can reasonably expect material science/chemistry graduates to be the hot talent property of the future.

- US shale oil production has exploded in recent years. Investment, employment and GOP election coffers have all benefitted. Oil prices, even if they recover back to the $30 levels, make shale oil an uneconomic proposition. US oil producing states are mainly Republican voting states but jobless voters can be fickle. It might be tough for them to stomach a Democrat President but it seems the current White House incumbent believes they can stomach disinfectant. So, anything is possible in the November election.

As always, human beings are not great at forecasting the future. However, it is a racing certainty that the oil markets have not exhausted their ability to deliver further shocks in 2020.

Enjoyed this blog? Then why not check out our other great content by clicking here!