More than 60,000 candidates will sit the Leaving Certificate next week. The parents of these children will understandably be anxious as to how they fare in the race for prized places in third level education but such anxiety is possibly a wee bit misplaced.

As recently as 1980 just 20% of secondary school leavers went on to third level education, but that figure is now well over 60% suggesting opportunities to maximize career potential have risen exponentially for our children. Possibly not.

A cursory glance at financial markets would suggest that educational uncertainty should now be replaced by career uncertainty.

The S&P 500 is a market index whose constituents are 500 of the largest companies in the US ranked by market capitalisation, or value in layman terms. This index is not set in stone and is subject to the forces of creative destruction. Companies drop off the list for one of two reasons; they can be the subject of corporate activity – buyouts, mergers, acquisitions – or they can fall below the market cap threshold and replaced by faster growing companies.

In the 1960s companies on average could expect an average tenure in the S&P 500 of 33 years. That average tenure shortened to 24 years in 2016 and is forecast by consultancy, Innosight, to shrink to an incredible 12 years by 2027.

The acceleration in longevity decline is not the result of increased corporate activity but by the rapid evolution of technology and the structural destruction of many industries. Think railroads of the 1950s, newspapers and retailers in the 2000s. This the challenge facing the graduates of tomorrow – trying to avoid career paths which meet sector obsolescence. Energy is the future, right? That depends….

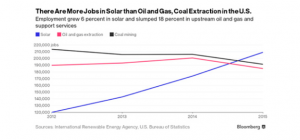

Despite Mr Trump’s love affair with “beautiful clean coal” there is a structural shift in employment in the energy sector which might surprise. The number of US jobs in solar energy overtook those in oil and natural gas even before the current President came to power. The chart below is fairly striking:

Readers might also be surprised to know that despite Trump’s big oil support, Iran tensions, healthy global growth, record market(S&P) highs and the post-Fukushima decline in nuclear power, the largest quoted oil company in the world, Exxon Mobil, has experienced a 25% decline in its share price since solar took top jobs spot in 2015.

Very often a multi-year slippage in the relative value of a sector in an index can signal a structural decline for an industry(sector). Take a look at the long term charts of companies in retail, media, telecoms and financial services’ sectors and you will see more losers than winners. These are the victims of creative destruction wrought by new digital technologies.

A current check of the weightings of sectors in the S&P 500 is also instructive.

The technology sector accounts for more than 25% of total S&P 500. No doubt many of these companies will have their own risks of technological obsolescence but spare a thought for the financial sector which once accounted for more than 20% of the index. It currently sits below 15% and that’s when financial conditions are at the most benign this planet has ever experienced.

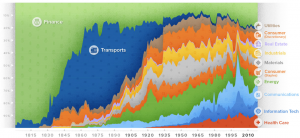

A quick tot up of S&P structurally exposed sectors like energy, utilities, financials, retail and communications can readily account for more than a third of the market right now. This figure may resonate with market historians who will know that transport(railroads) accounted for 38% of the US stock market in 1900. Today it is 2%.

The following stunning graphic from Visual Capitalist illustrates the shifty in sector significance over 200 years:

Clearly, humans are not great at forecasting the future but it is safe to say technology will be a significant part of the lives of the leaving class of 2019.

Perhaps the more pragmatic approach is to build knowledge and skills rather than commit to a specific industry. More particularly think about working with technology rather than in technology.

A recent Accenture report highlighted the challenge for employers meeting a skills crisis but also provided a reasonable guide to under-graduates as to where employers will look in the future:

“To many, the response to the skills crisis is simple: train more engineers; raise the number of arts graduates. But creating larger cohorts with certain skills is not the answer. Two things stand out in our analysis:

- Creativity, socio-emotional intelligence and complex reasoning are the skills that are rising in importance across every work role. These skills are not taught in today’s learning systems. They are acquired through practice, experience and often over long-time periods.

- The blend of skills required by each worker is becoming more complex. There needs to be a greater emphasis on broadening the variety of skills within each worker.”

Another useful guide to the skills required of the next generation is to look at the founders of start ups in today’s world. They tend to be creative thinkers, technology-savvy and articulate communicators of their vision. Furthermore, the sectors where start ups are focusing can give a good guide to our children’s future. For the anxious parents out there you might consider going to a few EIIS start-up presentations and getting a sense of the skills and sectors which are likely to feature in your own childrens’ careers…..