Hoo boy. Boris Johnson singing “I Will Survive” to his new communications chief was not on my Monday morning bingo card. My money is on a Doors soundtrack soon enough but let’s turn to real money and financial services. As Revolut announces a further push into the personal finance space in Ireland I couldn’t help thinking of the survival chances of traditional financial players.

A recent personal interaction with a large European player in the pensions space was instructive. My simple transaction request in the middle of last month apparently missed the January “roll” but I was reassured that it would make the next “roll” on the last day of February. No, seriously. There are no words, just a wall of capital flooding into fintech. The numbers are staggering and should scare the hell out of incumbent financial players. Check out the following developments:

- Fintech funding acceleration: Global fintech funding reached $132 billion across 4,969 deals in 2021. That’s a 168% increase on 2020. In fact, $1 out of every $5 of venture funding went to fintech in 2021(source: CB Insights).

- Unicorn creation: It’s not just Wayflyer grapping $1 billion valuation(unicorn) status. Actually, in the world of fintech the pace of unicorn creation is mighty – CB Insights have reported 157 fintech unicorn “births” in 2021 which equates to more than three a week!

- Finance-as-a-Service: We deliberately mentioned Wayflyer earlier. Its ’edge’ and part of its service is marketing analytics expertise for e-commerce companies. However, it is in reality a financing company which provides funds in an innovative way to help grow businesses. Its funding decisions are super-quick, require only 6 months of trading by the customer and pay-back is based on revenues which can slow or accelerate depending on growth trajectory. Imagine having that type of arrangement with a traditional banking entity!

- Capital critical mass: The value of fintech start ups reached $3.5 trillion in 2021 (source: Dealroom.co). For context, that’s a bigger capital value than the entire publicly listed energy sector! There are now more than 433 unicorns(> $1 billion value) in fintech. To this writer, fintech has reached investment critical mass. The really big money has decided fintech is going to squeeze out most traditional players. And the big capital centres are seeing the future too…..

- New York crypto: The Big Apple is currently the crypto capital of the US. More than $6.5 billion, or 46%, of total crypto funding went to New York in 2021(source: CB Insights). But, it’s not just traditional US financial centres ramping up the fintech revolution…

- London leading: The UK is an easy target for derision when the PM is described as “not a complete clown”. That’s the new communications chief, not me. Back to the non-parody world, the UK fintech story is undeniably impressive and, in a rare visit of credibility to London, can be supported by facts. UK fintech investment grew 617% (that’s almost 7-fold) to £27 billion in 2021(Source: Bloomberg).

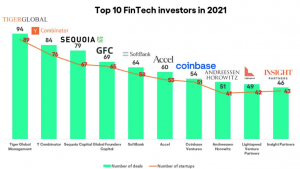

Yes, it is entirely possible there will be poor investments made and capital destroyed. I note that sales of superyachts are tracking fintech funding growth rather too closely for comfort – CB Insights reporting a 77% surge in 2021. However, one can’t help noticing some very credible VC players rapidly increasing their fintech profile. The chart below (source: Medici) highlights Tiger Global, Y Combinator and Sequoia doing almost two fintech deals….. per week.

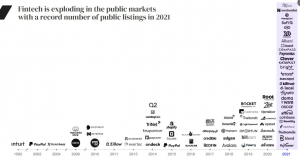

And there are exits too. Last year’s IPO explosion was helpful for fintech listings in this logo graphic from Capital IQ:

Of course, there will be winners and losers, just like there were in the TMT 2000 days. However, the sheer size of the $3.5 trillion fintech revolution makes it a racing certainty the Amazon or Google of future finance will emerge from this pool of talent and technology. I’m also sure the next significant technology “roll” for the pensions clown show will be The End.