Would your business accept payment in a cryptocurrency? You might have to consider this question a bit sooner than expected. The extreme volatility of Bitcoin and other crypto challengers would correctly give the impression that such payments would be a commercial risk requiring a rather strong stomach. However, Facebook’s recently announced plans to launch a new digital currency, Libra, is a potential game changer and has prompted serious consideration from unlikely quarters.

The Bank for International Settlements(BIS) is the bank used by central bankers and would be perceived as a bastion of conservative thinking and risk aversion. So, it is noteworthy to hear BIS bank head Agustin Carstens admit that “it might be… sooner than we think that there is a market and we need to be able to provide central bank digital currencies”. Bitcoin has been with us for ten years so why has Facebook’s move caught the attention of central bankers? Clearly, the entry of big tech into financial services raises some serious strategic issues for incumbent banks already struggling with their own technology transitions. However, there are two other aspects to the Facebook initiative which suggest a viable digital currency could be a genuine business banking consideration sooner rather than later.

Firstly, Facebook is addressing the business-killing problem of extreme volatility in cryptocurrencies. Libra’s value will be stabilised by backing it with real world financial assets drawn from liquid pools of bank deposits and short term government securities denominated in a variety of hard currencies eg. USD, JPY, GBP and EUR. This should result in a “stable coin” with reduced fluctuations compared to the local currencies used by consumers and businesses.

Second, a credibility problem surrounding cryptocurrencies has been the lack of institutional reputation or trust being put on the line. In a nutshell, governance and validation are critical to mainstream adoption. The striking thing about Facebook’s approach is the international partnerships established with 100 validators to ensure neutrality and trust in the running of the Libra network(Blockchain). The Libra Association will base itself in Switzerland and has already secured 27 founding partners including the likes of Visa, Paypal, Uber, Vodafone, Stripe, and eBay. If one can park current concerns regarding Facebook’s extraordinary data control over 2.5 billion consumers, Libra looks like a serious prospect as a global digital currency.

This article does not propose to look at the technology issues but, given Facebook’s execution track record, we can assume their plans to use a combination of existing blockchain technologies will deliver a stable digital currency in 2020. If one re-reads the BIS quote above one senses central banks know its going to happen and are preparing for the creation of their own digital currencies. This raises a number of fundamental considerations as currency/legal tender underpins the commercial activities and financial instruments used across the global economy. The traditional banking system and central bank/ BIS should not assume a counter initiative in digital currencies will necessarily restore some sort of influence parity.

A clue as to traditional banking concern over the control of the foundation block of the financial system is the just published BIS Annual Economic Report and its prominent Section III – “ Big Tech in Finance: Opportunities and Risks”. While it recognizes the entry of technology firms into financial sevices as a positive for efficiency gains and potential inclusion of the “unbanked” 30% of the world’s population the report also focuses on “new and complex trade-offs between financial stability, competition and data protection”. The reality for central banks is that technology firms have huge user bases, a commensurate stock of massively rich user data which is utilized to offer services that exploit network effects, generating further usage and even more data to drive activity. In a previous article on Internet Trends we highlighted the case of Chinese giant, Alipay, which already has a billion users and provides financial services to hundreds of millions of customers. Think Facebook and its 2.5 billion user network.

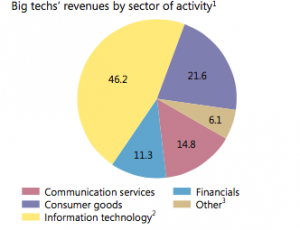

Already commentators are focusing on the potentially rapid evolution of Facebook into a dominant financial services player. It’s early days yet and the BIS report points out that big tech currently only derives 11% of its revenues from finance as seen in the following chart:

Given currency’s position as the commercial foundation of modern civilization and commerce there is a fascinating article in Wired which perhaps reveals the true concerns of traditional banking institutions, policy makers and regulators. The following passage in the article was perhaps the most provocative:

“And while Facebook’s ambitions appear unsubtle (at least to me), the biggest tech companies are all building more and more advanced and immersive ecosystems. So maybe it’s time to start asking: What is the functional difference between a company and a country?

It’s not a crazy question: We’re already at a point where huge multinational tech monopsonies have so much power over the global economy that central bankers and regulators are starting to wonder if they even have the tools to set economic policy, like they used to in the old days.

And the reason these big tech companies are different from other giant multinational corporations like Exxon Mobile or ConAgra or even, strangely, Microsoft is that their ambition really is to own all your interactions, not just your driving or your eating or your typing.”

Wowzers. Facebook or Google achieving country-like status with control and influence over monster populations, or user bases, and revenues in excess of the GDPs of most countries on the planet. No wonder the bankers are looking to wrest back control before it’s too late. BIS head of research Hyun Song Shin does little to hide the fact that Facebook’s Libra has moved the risk dialsignificantly – “ ..there is a need for international cooperation on rules and standards. The recent proposal by Facebook to launch a digital currency, Libra, has underscored the importance of cross border cooperation.” Yes, the regulatory stick is being waved already. Indeed, even the US Senate Banking Committee is sitting up and taking notice; a hearing on Libra is scheduled this month while various European politicians have voiced concerns about the emergence of a Facebook “shadow bank” with a user base vastly bigger than Europe’s 600 million population. The euro under pressure from Italian mini-BOT proposals, plunging negative interest rates and pending Brexit trade chaos can ill-afford another existential threat.

Traditional players won’t be the only ones seeing a threat. It is highly unlikely that Amazon, Google or Apple will stand idly by. All three have rolled out their own payment options as their users have become comfortable with digital commerce. Interestingly, a country which has effectively gone almost cash-less is also moving quite rapidly towards a digital version of its currency.

Sweden’s central bank, the Riksbank, is fully aware that only 13% of the population has carried out a recent transaction in cash. Four out of every five purchases in Sweden are made electronically and the Riksbank can see where this is going. Hence, they have launched a pilot project to develop and test a technology solution for an “e-krona”. This pilot is generating plenty of domestic controversy as a potential state-like interference from the Riksbank in private commerce. The future of the e-krona is more than uncertain but the digital genie is out of the banking bottle. Central bankers are clearly assuming big tech is going to enter and disrupt the financial ecosystem.

Business owners will need to watch digital currency developments carefully and prepare for relatively quick adoption. Think back to all the lost revenues(and franchises) of retailers slow to embrace e-commerce and online payment facilities/technologies. Of course, there will be sceptics. None more famous than the world’s most powerful commercial banker, Jamie Dimon of JP Morgan. As recently as November 2015 Dimon said Bitcoin, trading at $400 at the time, would not survive. Well, almost ten years after its launch Bitcoin is still with us and trading around $10,000. We would tend to agree with Dimon that the technology(blockchain) is more sustainable than Bitcoin but there was more than a hint of irony in February this year when JP Morgan launched its own cryptocurrency – “JPM Coin” – for its clients. The bankers’ message is clear.

Digital currencies are coming to mainstream commercial activities. Big Tech is the catalyst forcing banking responses including actual crypto solutions. Businesses will need to pay attention as they most likely will have to be digital-ready quite soon….