As I flicked through the quarterly results of JP Morgan and Citigroup this week I was reminded that in some ways the whole future of the financial system lies in my brother’s hands. He currently works for another monster bank and there’s a part of me which hopes he will leave banking for all our sakes. Perhaps I’m over-egging this career wish but the previous four banks for which my grim reaper-relative worked all went bust. The world can’t afford a sudden megabank failure. The good news, for now, is that things in the near term big banking world are pretty strong.

Despite some gloomy predictions for the future of banking, JP Morgan just posted the most profitable year in the history of US banking. This makes it increasingly likely the record total $111 billion profits made by the big 6 US banks in 2018 will be beaten in the next few weeks as 2019 joins the reporting history books. Regular readers are certainly familiar with the challenges to traditional banks posed by technology transitions and even Big Tech competition. However, it is still possible banks will not disappear but rather change their interface with customers.

We recently wrote in our article “Are You Ready For Change?” that finance would probably become “a feature” of most products and services but would no longer be accessed as a standalone access point:

“If we recall the pre-Amazon era, consumer spend and logistics were separate activities. Now, delivery is a feature of consumer spend from Christmas trees to sushi. In the world of finance, it is quite likely payments and financial services will be embedded features of other services rather than standalone banking. Prepare for “location” banking to die.”

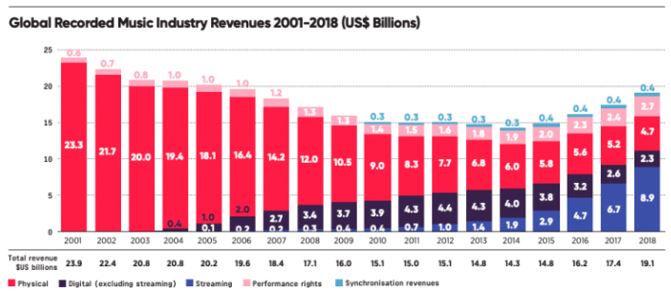

This prompted some thought as to whether there were any analogous experiences in another industry. Well, it has become mainstream thinking these days that banking is facing a technological music with which it might struggle for relevancy. So, let’s look at the music industry. As recently as 2014 the death knell of the industry was sounded with global recorded music revenues collapsing by 25% from $19.6 billion to $14.3 billion since 2006.

The revenues from physical music alone in 2006 were worth $16.4 billion. The doomsdayers were correct. Physical music revenues have fallen a further 75% but there was no such thing as “streaming” back in 2006. Now, music streaming revenues account for more than 50% of global music revenues. Here’s the comeback graphic:

So let’s hold that “streaming” thought for the banking industry. It is entirely possible there will be new channels for banks to deliver core services. We should be watching activity in the “plumbing” of financial services for clues to the future. Interestingly, this week we witnessed a very big fintech deal with Visa Inc agreeing to purchase fintech start-up Plaid for…. $5.3 billion.

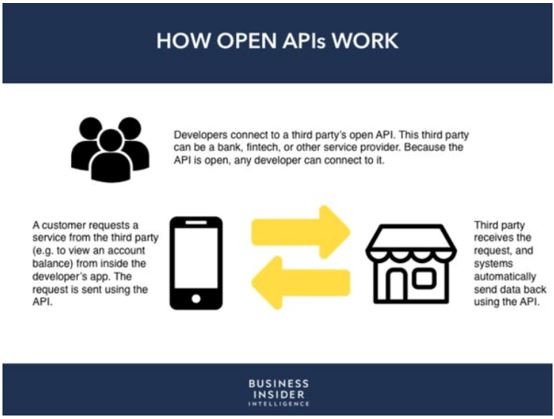

For perspective, Plaid raised $250m in a Series C funding round barely more than a year ago at a $2.65 billion valuation. Plaid is a “plumbing” or “streaming” play as it allows consumers to connect their bank accounts to various 3rd party services from wealth manager robo-advisors to insurance. The technology which allows this connectivity is Application Programming Interfaces, or APIs. The following graphic shows how APIs work:

Clearly, Visa Inc sees the value of owning the plumbing which is connecting the latest fintech to traditional bank accounts. Note this deal does not preview a world where bank accounts disappear. Perhaps current thinking is too negative on the future of banking? Music could be the inspiration, and ironically music featured in our last banking crisis. It was a rather unfortunate quote from a Citigroup CEO in 2007 who insisted “as long as the music (liquidity) is playing, you’ve got to get up and dance”. Well, the music stopped too quickly for Chuck Prince and many other failed banks.

Technology is the current gloomy soundtrack for banking but “streaming” and APIs provide potential recovery and a future. Now, all we have to do to ensure planetary financial survival is persuade my brother to take up the guitar full time…..